South Africa vs USA: A Tale of Two Interest Rate Paths

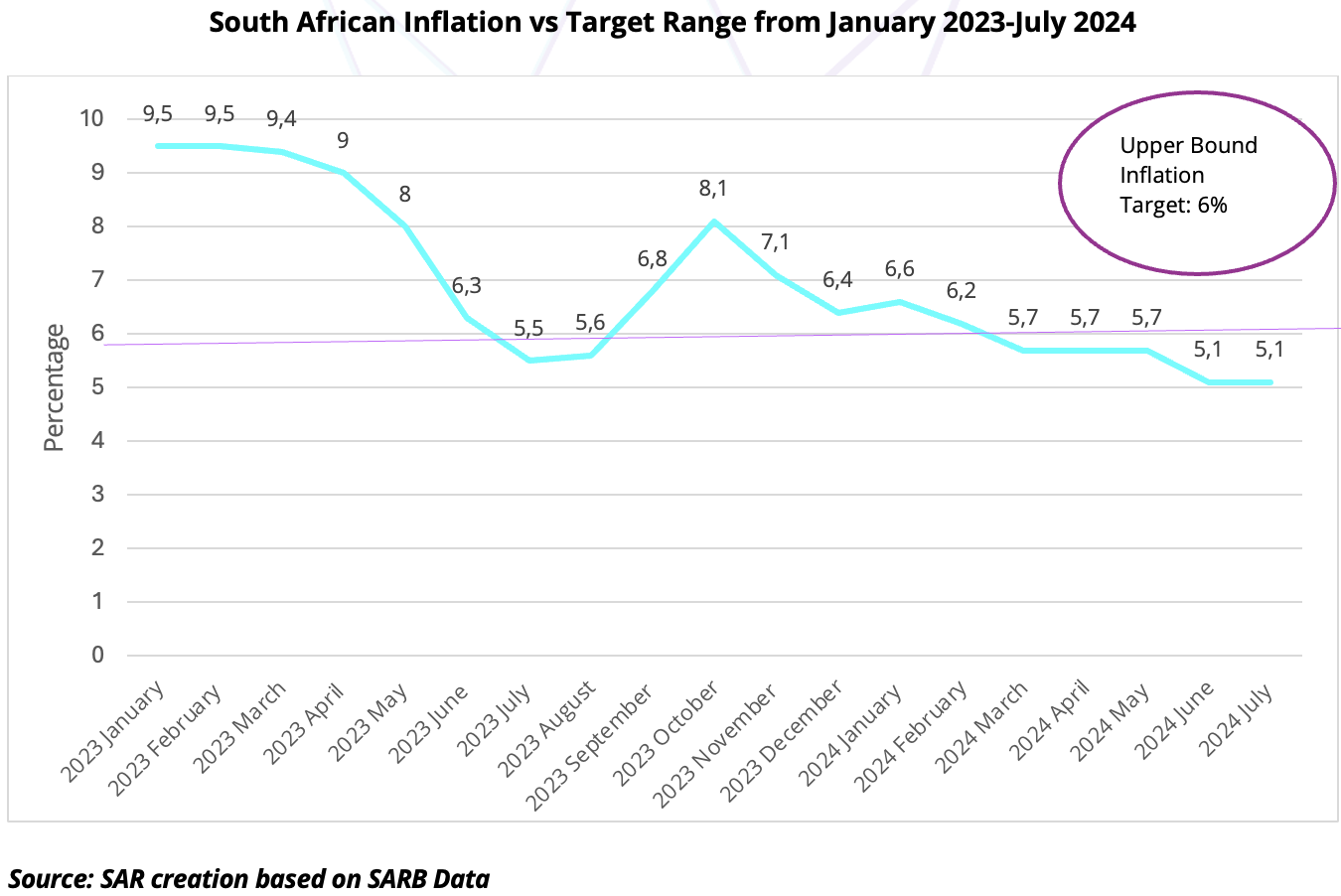

A Cautious Approach Amidst Economic PressuresSouth Africa finds itself in a delicate balancing act as it grapples with persistent inflation and a sluggish economy. The Reserve Bank has maintained a hawkish stance, prioritising inflation control over economic growth. While inflation has shown signs of moderation, it remains in the higher level of its target range of 3-6%, with the latest reading at 5.1% in June 2024, limiting room for significant interest rate cuts.

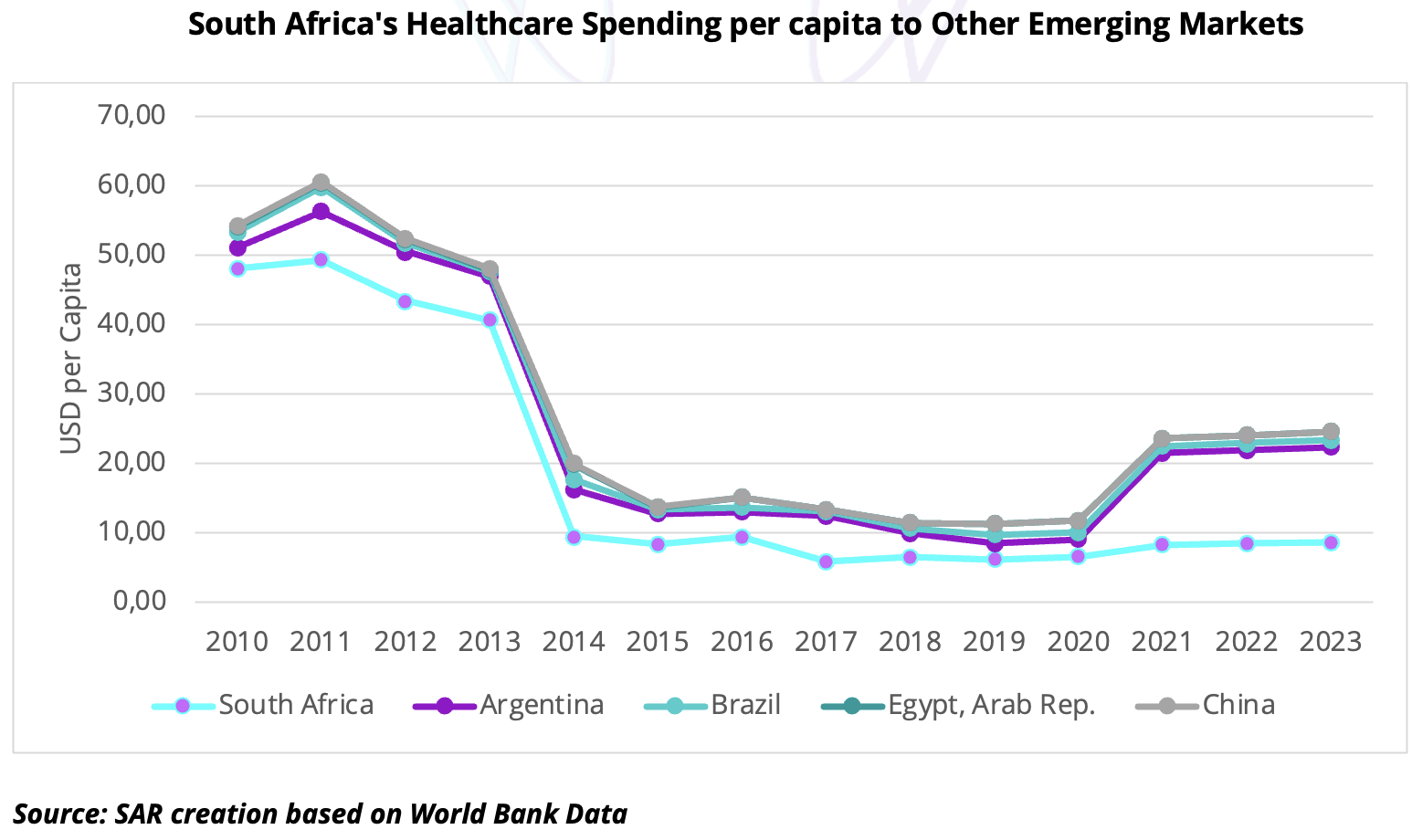

There is optimism that interest rates may be lowered soon, with expectations for a significant cut. Although the Monetary Policy Committee recently opted to maintain the current high interest rate, there were dissenting opinions advocating for a reduction. Since 2021, interest rates have been raised substantially to combat inflation.Looking ahead, inflation is projected to align more closely with the central bank’s target by late 2024, indicating a positive shift. Additionally, the local currency has gained strength following recent political changes, which may further influence economic stability.South Africa's unemployment rate remains stubbornly high at 34% as of the second quarter of 2024, indicating a significant skills mismatch and labour market challenges. The country's government debt-to-GDP ratio has been on an upward trajectory, reaching 71.4% in 2023. The trade balance has shown a deficit in recent quarters, highlighting the country's reliance on imports and vulnerability to global economic shocks. Foreign direct investment (FDI) inflows have been relatively modest, indicating a need to improve the investment climate to attract more foreign capital.An interest rate cut could stimulate economic growth and job creation, potentially addressing the high unemployment rate. However, the impact on income inequality and poverty might be limited without complementary social policies. While lower borrowing costs could benefit businesses and consumers, it is essential to ensure that the benefits are distributed equitably. Additionally, an interest rate cut might exacerbate inflationary pressures if not accompanied by supply-side reforms to boost productivity and competitiveness.South Africa's education and healthcare spending per capita remains relatively low compared to global standards. Increased access to quality education and healthcare is crucial for long-term economic growth and social development. While an interest rate cut might provide some short-term relief, sustained investment in these sectors is essential for addressing deep-rooted challenges and improving living standards. Moreover, expanding access to financial services can empower individuals and businesses, contributing to economic growth and stability.

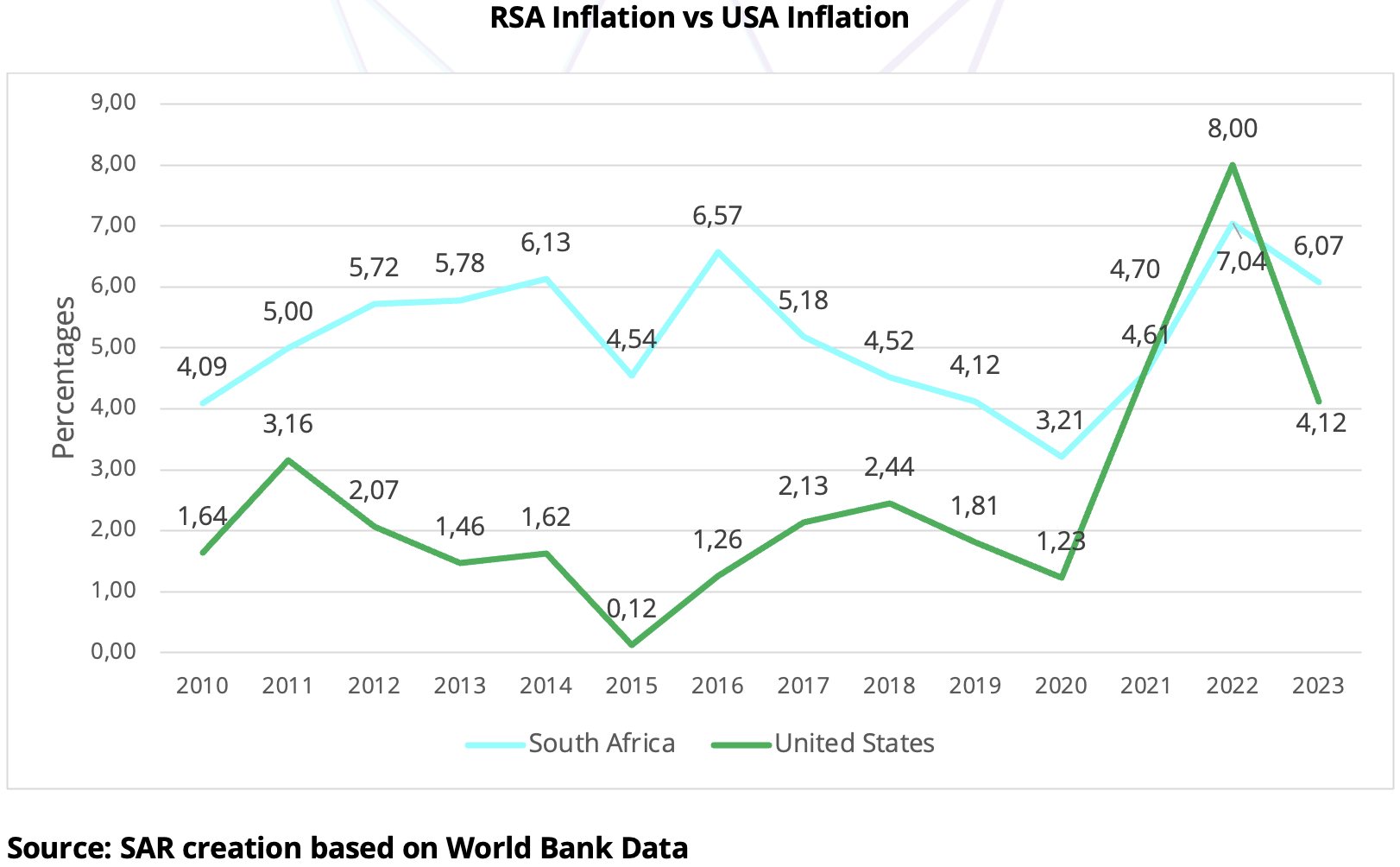

Persistent high unemployment, rising government debt, and a widening trade deficit pose significant challenges to South Africa's creditworthiness. While an interest rate cut could provide some short-term relief, it is unlikely to address the underlying structural issues.InflationSouth Africa's credit profile is notably weaker than the United States'. The country has consistently grappled with higher inflation rates, averaging around 6-7% in 2024, compared to the US' projected 3-4%. This disparity is largely attributable to structural economic challenges, such as supply-side constraints and exchange rate volatility, which are less pronounced in the US economy.Beyond inflation, South Africa's unemployment rate remains significantly elevated at approximately 34%, dwarfing the US' unemployment rate of around 4%. Moreover, GDP growth projections for South Africa are more modest compared to the US.These macroeconomic disparities exert pressure on South Africa's creditworthiness. The South African Reserve Bank operates in a more challenging environment, balancing the need to control inflation with the imperative to stimulate economic growth. In contrast, the US Federal Reserve has more policy flexibility due to a generally more robust economic backdrop.

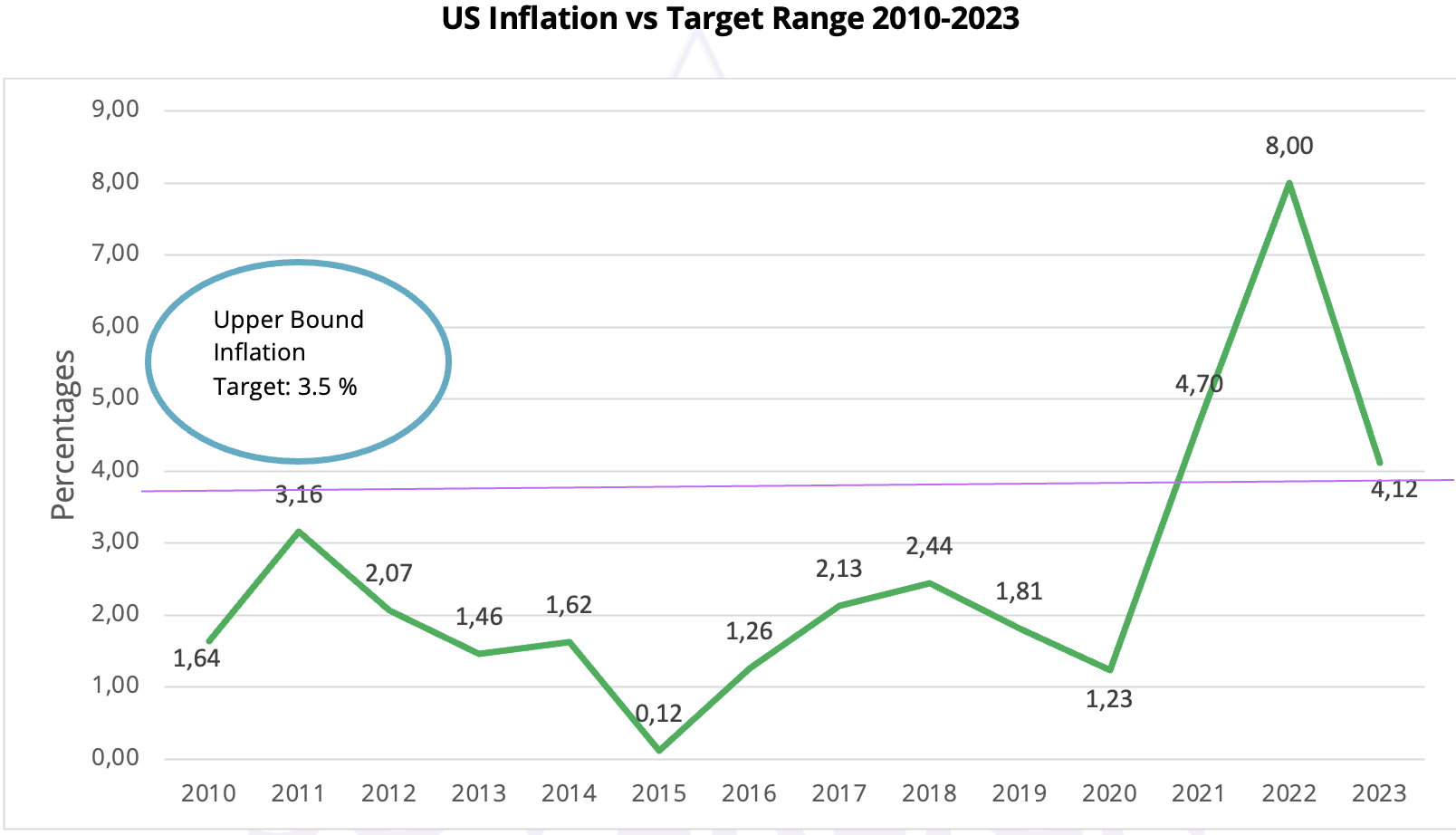

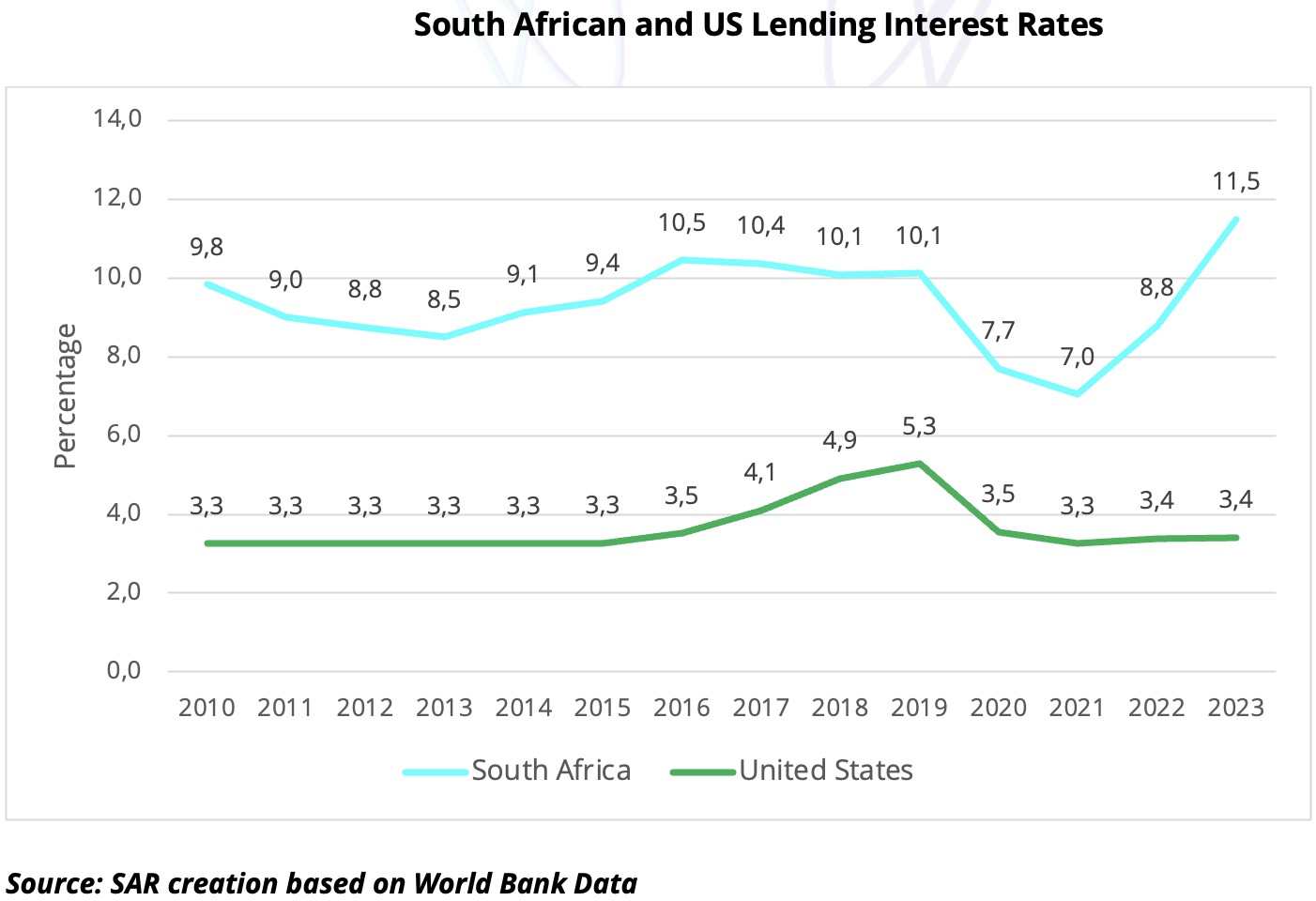

Bond Market and Stock MarketAs of 2024, the US economy exhibits a more benign landscape with inflation hovering around 3.5%, allowing the Federal Reserve to adopt a less restrictive monetary policy. This, coupled with the central bank's benchmark interest rate range of 5.25% to 5.50%, has fostered a stabilising equity market, as evidenced by the S&P 500's positive trajectory.In contrast, South Africa faces a steeper inflationary challenge, necessitating a more aggressive monetary stance from the South African Reserve Bank. The resulting prime lending rate of 8.25% has amplified volatility in the bond market due to heightened inflation concerns and underlying structural economic weaknesses. The JSE has mirrored these challenges, though certain sectors have shown resilience.These divergent economic conditions highlight the imperative for investors to adopt a diversified approach. Prudent portfolio management across various asset classes and geographic regions is essential to navigate the complexities of differing inflationary pressures and interest rate environments.USA: A Potential Pivot and Its ImplicationsIn contrast to South Africa, the United States is on the cusp of a potential interest rate cut. The Federal Reserve, after a series of aggressive rate hikes to combat inflation, is now signalling a shift in its monetary policy stance. Declining inflation, with the latest CPI reading at 3% in June 2024, and a softening labour market have paved the way for a more accommodative approach. The US economy expanded by 2.2% in 2023, and forecasts suggest a growth rate of 1.8% in 2024.

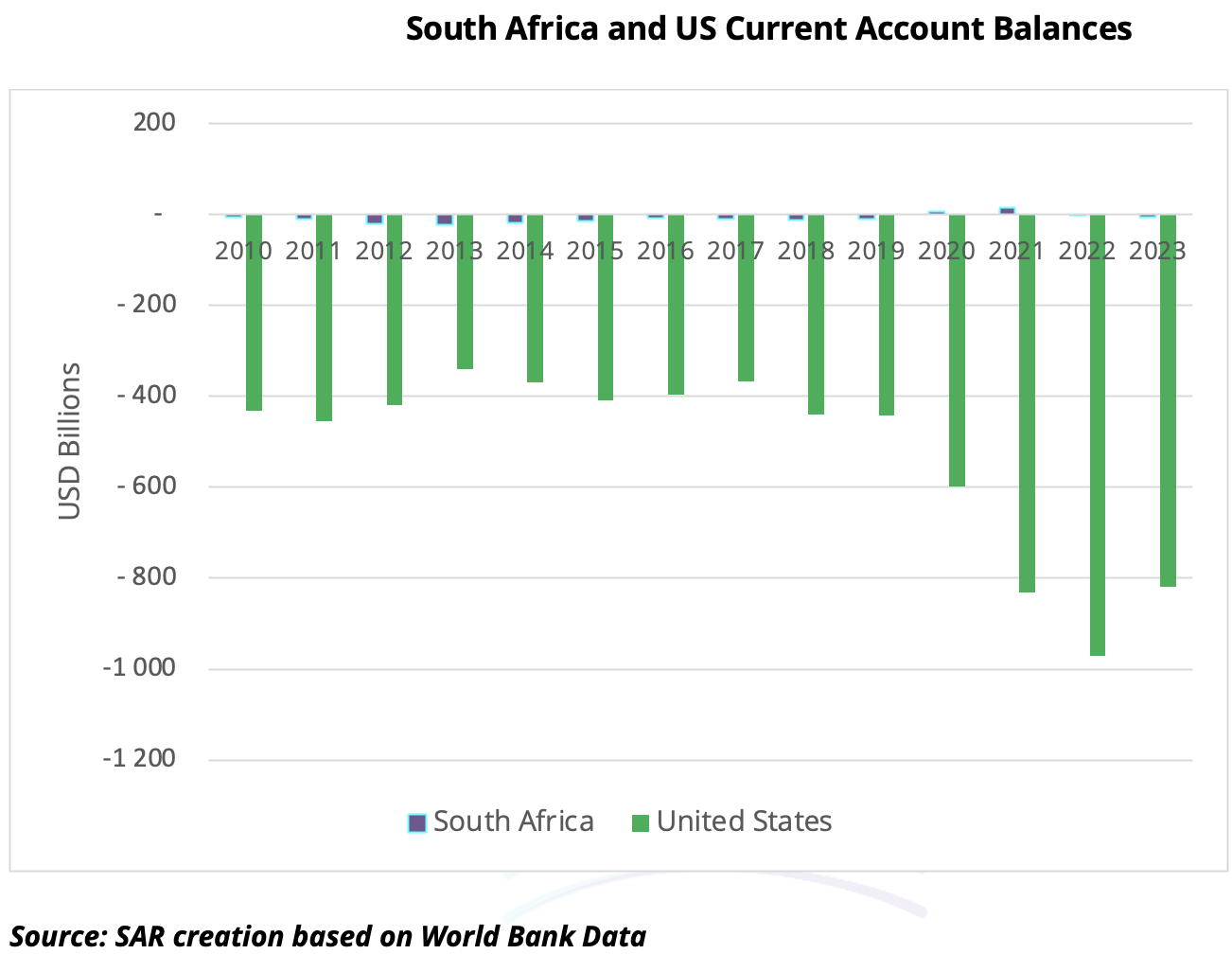

A rate cut in the US is expected to stimulate economic activity and potentially boost consumer spending. However, the magnitude and timing of these cuts remain uncertain, influenced by evolving economic data and geopolitical developments.The US unemployment rate declined to 3.6% in June 2024, indicating a tight labour market. Government debt levels remain high but have shown signs of stabilisation. The trade deficit has widened in recent quarters, reflecting strong domestic demand and a reliance on imports. Despite economic uncertainties, the US continues to attract significant FDI inflows, supported by its large market size and stable political environment.While the US has made progress in reducing poverty, income inequality remains a persistent challenge. An interest rate cut could stimulate economic growth and job creation, potentially benefiting lower-income households. However, the impact on income inequality might be limited without targeted policies to address wealth distribution. Moreover, a rate cut could exacerbate asset price inflation, widening the wealth gap.The US boasts a relatively high level of education and healthcare spending per capita. However, disparities in access to quality education and healthcare persist, particularly among marginalised communities. An interest rate cut could indirectly support these sectors by stimulating economic growth and increasing government revenue. However, targeted investments and policy reforms are essential to address underlying challenges and ensure equitable access to essential services. The US financial system is relatively well developed, with high levels of financial inclusion. Nevertheless, efforts to expand access to financial services for underserved populations, such as low-income households and small businesses, remain crucial for promoting economic growth and stability.A declining inflation rate, a robust labour market, and a stable political environment contribute to a positive credit outlook for the United States. However, persistent income inequality and challenges in certain sectors require ongoing policy attention.The Broader ImpactThe divergence in monetary policy between South Africa and the US will have implications for various sectors. For instance, a steeper rate cut trajectory in the US could lead to capital outflows from emerging markets like South Africa, exerting downward pressure on the rand. The rand has depreciated by approximately 10% against the US dollar since the beginning of 2024.Furthermore, the differential in interest rates can impact trade flows and investment decisions. A widening interest rate gap might incentivise investors to seek higher returns in the US, potentially affecting capital inflows into South Africa. The South African current account deficit widened to 2.8% of GDP in the first quarter of 2024, reflecting increased imports and lower export earnings.

Credit Rating ImplicationsSouth Africa's credit rating is likely to remain under pressure due to persistent economic challenges, including high unemployment, rising government debt, and a widening trade deficit.The US credit rating is generally considered to be strong, supported by a diversified economy, a stable political environment, and a history of fiscal discipline. However, rising government debt levels and persistent income inequality pose medium-term risks to the credit profile.In conclusion, the differing economic strategies of the US and South Africa illustrate the complexities of managing monetary policy in varying contexts. The US, poised for interest rate cuts, benefits from a stronger economic foundation, allowing for greater flexibility in fostering growth while ensuring credit stability. Conversely, South Africa's caution reflects ongoing inflation and structural challenges, indicating that while rate cuts could temporarily alleviate some pressures, they won't resolve deeper issues such as high debt and unemployment without further reforms. This divergence underscores the need for each country to tailor its economic policies to address unique challenges, balancing the pursuit of growth with the imperative of financial stability to secure long-term prosperity.

There is optimism that interest rates may be lowered soon, with expectations for a significant cut. Although the Monetary Policy Committee recently opted to maintain the current high interest rate, there were dissenting opinions advocating for a reduction. Since 2021, interest rates have been raised substantially to combat inflation.Looking ahead, inflation is projected to align more closely with the central bank’s target by late 2024, indicating a positive shift. Additionally, the local currency has gained strength following recent political changes, which may further influence economic stability.South Africa's unemployment rate remains stubbornly high at 34% as of the second quarter of 2024, indicating a significant skills mismatch and labour market challenges. The country's government debt-to-GDP ratio has been on an upward trajectory, reaching 71.4% in 2023. The trade balance has shown a deficit in recent quarters, highlighting the country's reliance on imports and vulnerability to global economic shocks. Foreign direct investment (FDI) inflows have been relatively modest, indicating a need to improve the investment climate to attract more foreign capital.An interest rate cut could stimulate economic growth and job creation, potentially addressing the high unemployment rate. However, the impact on income inequality and poverty might be limited without complementary social policies. While lower borrowing costs could benefit businesses and consumers, it is essential to ensure that the benefits are distributed equitably. Additionally, an interest rate cut might exacerbate inflationary pressures if not accompanied by supply-side reforms to boost productivity and competitiveness.South Africa's education and healthcare spending per capita remains relatively low compared to global standards. Increased access to quality education and healthcare is crucial for long-term economic growth and social development. While an interest rate cut might provide some short-term relief, sustained investment in these sectors is essential for addressing deep-rooted challenges and improving living standards. Moreover, expanding access to financial services can empower individuals and businesses, contributing to economic growth and stability.

Persistent high unemployment, rising government debt, and a widening trade deficit pose significant challenges to South Africa's creditworthiness. While an interest rate cut could provide some short-term relief, it is unlikely to address the underlying structural issues.InflationSouth Africa's credit profile is notably weaker than the United States'. The country has consistently grappled with higher inflation rates, averaging around 6-7% in 2024, compared to the US' projected 3-4%. This disparity is largely attributable to structural economic challenges, such as supply-side constraints and exchange rate volatility, which are less pronounced in the US economy.Beyond inflation, South Africa's unemployment rate remains significantly elevated at approximately 34%, dwarfing the US' unemployment rate of around 4%. Moreover, GDP growth projections for South Africa are more modest compared to the US.These macroeconomic disparities exert pressure on South Africa's creditworthiness. The South African Reserve Bank operates in a more challenging environment, balancing the need to control inflation with the imperative to stimulate economic growth. In contrast, the US Federal Reserve has more policy flexibility due to a generally more robust economic backdrop.

Bond Market and Stock MarketAs of 2024, the US economy exhibits a more benign landscape with inflation hovering around 3.5%, allowing the Federal Reserve to adopt a less restrictive monetary policy. This, coupled with the central bank's benchmark interest rate range of 5.25% to 5.50%, has fostered a stabilising equity market, as evidenced by the S&P 500's positive trajectory.In contrast, South Africa faces a steeper inflationary challenge, necessitating a more aggressive monetary stance from the South African Reserve Bank. The resulting prime lending rate of 8.25% has amplified volatility in the bond market due to heightened inflation concerns and underlying structural economic weaknesses. The JSE has mirrored these challenges, though certain sectors have shown resilience.These divergent economic conditions highlight the imperative for investors to adopt a diversified approach. Prudent portfolio management across various asset classes and geographic regions is essential to navigate the complexities of differing inflationary pressures and interest rate environments.USA: A Potential Pivot and Its ImplicationsIn contrast to South Africa, the United States is on the cusp of a potential interest rate cut. The Federal Reserve, after a series of aggressive rate hikes to combat inflation, is now signalling a shift in its monetary policy stance. Declining inflation, with the latest CPI reading at 3% in June 2024, and a softening labour market have paved the way for a more accommodative approach. The US economy expanded by 2.2% in 2023, and forecasts suggest a growth rate of 1.8% in 2024.

A rate cut in the US is expected to stimulate economic activity and potentially boost consumer spending. However, the magnitude and timing of these cuts remain uncertain, influenced by evolving economic data and geopolitical developments.The US unemployment rate declined to 3.6% in June 2024, indicating a tight labour market. Government debt levels remain high but have shown signs of stabilisation. The trade deficit has widened in recent quarters, reflecting strong domestic demand and a reliance on imports. Despite economic uncertainties, the US continues to attract significant FDI inflows, supported by its large market size and stable political environment.While the US has made progress in reducing poverty, income inequality remains a persistent challenge. An interest rate cut could stimulate economic growth and job creation, potentially benefiting lower-income households. However, the impact on income inequality might be limited without targeted policies to address wealth distribution. Moreover, a rate cut could exacerbate asset price inflation, widening the wealth gap.The US boasts a relatively high level of education and healthcare spending per capita. However, disparities in access to quality education and healthcare persist, particularly among marginalised communities. An interest rate cut could indirectly support these sectors by stimulating economic growth and increasing government revenue. However, targeted investments and policy reforms are essential to address underlying challenges and ensure equitable access to essential services. The US financial system is relatively well developed, with high levels of financial inclusion. Nevertheless, efforts to expand access to financial services for underserved populations, such as low-income households and small businesses, remain crucial for promoting economic growth and stability.A declining inflation rate, a robust labour market, and a stable political environment contribute to a positive credit outlook for the United States. However, persistent income inequality and challenges in certain sectors require ongoing policy attention.The Broader ImpactThe divergence in monetary policy between South Africa and the US will have implications for various sectors. For instance, a steeper rate cut trajectory in the US could lead to capital outflows from emerging markets like South Africa, exerting downward pressure on the rand. The rand has depreciated by approximately 10% against the US dollar since the beginning of 2024.Furthermore, the differential in interest rates can impact trade flows and investment decisions. A widening interest rate gap might incentivise investors to seek higher returns in the US, potentially affecting capital inflows into South Africa. The South African current account deficit widened to 2.8% of GDP in the first quarter of 2024, reflecting increased imports and lower export earnings.

Credit Rating ImplicationsSouth Africa's credit rating is likely to remain under pressure due to persistent economic challenges, including high unemployment, rising government debt, and a widening trade deficit.The US credit rating is generally considered to be strong, supported by a diversified economy, a stable political environment, and a history of fiscal discipline. However, rising government debt levels and persistent income inequality pose medium-term risks to the credit profile.In conclusion, the differing economic strategies of the US and South Africa illustrate the complexities of managing monetary policy in varying contexts. The US, poised for interest rate cuts, benefits from a stronger economic foundation, allowing for greater flexibility in fostering growth while ensuring credit stability. Conversely, South Africa's caution reflects ongoing inflation and structural challenges, indicating that while rate cuts could temporarily alleviate some pressures, they won't resolve deeper issues such as high debt and unemployment without further reforms. This divergence underscores the need for each country to tailor its economic policies to address unique challenges, balancing the pursuit of growth with the imperative of financial stability to secure long-term prosperity.

0 Article Comments